Zumiez Inc. ZUMZ appears a preferred investors’ pick now, given its sound fundamentals and strategic efforts.

This renowned apparel, footwear, and accessories retailer seems well poised to capitalize on the trends in the apparel space, backed by its one-channel concept and advanced in-store fulfillment capabilities. ZUMZ has been making solid efforts for a while to meet robust demand with respect to distinct merchandise offering.

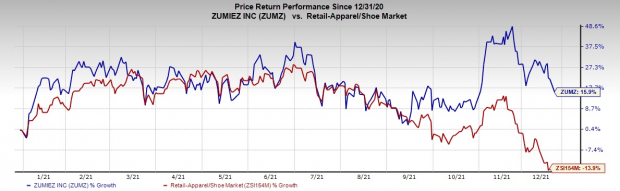

Shares of this Lynnwood, WA-based player have increased 15.9% against the industry’s 13.9% decline in the year-to-date period. This currently Zacks Rank #1 (Strong Buy) stock is further backed by its sturdy earnings estimate revisions. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for earnings currently stands at $4.97 for fiscal 2021 and $4.71 for fiscal 2022, mirroring growth of 7.3% and 10%, respectively. In fact, the Zacks Consensus Estimate for Zumiez’s current financial-year sales and earnings per share suggests growth of 20.3% and 63%, respectively, from the year-ago corresponding figures.

– Zacks

– Zacks Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Delving Into Strategies

Zumiez continues to gain from its one-channel approach and advanced in-store fulfillment capabilities, including Zumiez Delivery. ZUMZ’s focus on building a customer-centric business model, rooted in strong brands has been yielding results for sometime. Management also steadily exhibits prudent cost-management and strives to reduce shipping and fulfillment costs.

Zumiez is also focused on providing differentiated assortments. ZUMZ invested in resources to boost localized merchandising assortments. ZUMZ’s men’s, footwear and accessories categories are performing well. The implementation of advanced technology helped augmenting customers’ shopping experience across diverse channels. Further, ZUMZ is boosting competitive advantage by investing in logistics, planning and allocation along with omni-channel capabilities, which position it for growth over the long haul.

Coming to store-expansion efforts, Zumiez keeps up with the strategy of optimizing the store base through expansion in the underpenetrated markets while closing the underperforming ones. Also, a major proportion of its capital spending is allocated to store remodeling and openings. In fiscal 2021, management intends to open 23 stores comprising about seven in North America, 12 in Europe and four in Australia. Simultaneously, it plans to close nearly five to six outlets in the same period.

We believe, all the aforesaid strengths will tap incremental sales and continue boosting profits for Zumiez.

More Strengths

On its last earnings call, management cited that the fourth quarter of fiscal 2021 kicked off well. Zumiez provided details for the fiscal fourth quarter. The fiscal fourth quarter-to-date total sales for the 31 days ended Nov 30, 2021, climbed 11.5% from the same-period level ended Dec 1, 2020. Also, total net sales rose 8.6% from the same-period’s figure in fiscal 2019. Total comparable sales for the said 31-day period grew 8.4% year over year and 6.5% from the comparable period’s number in fiscal 2019. For the fiscal fourth quarter, Zumiez expects sales growth in high-single digits from the last fiscal year’s reported figure in the comparable quarter.

For fiscal 2021, Zumiez had projected net sales to improve in mid-teens from the fiscal 2019 actuals. This translates to net sales growth from the last fiscal-year levels to just above 20%. Gross margin is likely to grow substantially year over year, backed by leveraged occupancy costs on higher sales, lower shipping costs and increased product margins. Operating margins are estimated to grow year over year in reaching low-teens as a rate of sales.

Given all the discussed factors above, Zumiez is poised well for growth in the future and worth investing in.

Other Hot Stocks in Retail

Some other top-ranked stocks are Boot Barn Holdings BOOT, Tractor Supply Company TSCO and Target TGT.

Boot Barn Holdings, a lifestyle retailer of western and work-related footwear, apparel and accessories, sports a Zacks Rank #1 at present. The stock has jumped 142.8% in the year-to-date period.

The Zacks Consensus Estimate for Boot Barn Holdings’ current financial-year sales and earnings per share (EPS) suggests growth of 54.6% and 188%, respectively, from the year-ago corresponding figures. BOOT has a trailing four-quarter earnings surprise of 161.5%, on average.

Tractor Supply Company, a rural lifestyle retailer in the United States, currently flaunts a Zacks Rank of 1. TSCO has a trailing four-quarter earnings surprise of 22.8%, on average. Shares of TSCO have surged 58.1% year to date.

The Zacks Consensus Estimate for Tractor Supply Company’s current-year sales and EPS suggests growth of 19% and 23.9%, respectively, from the year-ago corresponding readings. TSCO has an expected EPS growth rate of 10.2% for three-five years.

Target, a renowned omni-channel retailer, presently carries a Zacks Rank #2 (Buy). TGT has a trailing four-quarter earnings surprise of 19.7%, on average. The stock has rallied 24.1% in the year-to-date period.

The Zacks Consensus Estimate for Target’s current-year sales and EPS suggests growth of 13.9% and 40.1%, respectively, from the corresponding year-ago levels. TGT has an expected EPS growth rate of 14.4% for three-five years.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Zumiez Inc. (ZUMZ): Free Stock Analysis Report

Target Corporation (TGT): Free Stock Analysis Report

Tractor Supply Company (TSCO): Free Stock Analysis Report

Boot Barn Holdings, Inc. (BOOT): Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research

What Makes Zumiez (ZUMZ) a Lucrative Investment Option Now

Source: Manila Trending PH

0 Comments